If you were hoping Southern California’s homebuying crash would finally turn around this year, it’s time to lower those expectations. A shaky economy, global conflict, stubbornly high home prices and expensive mortgages are still keeping buyers on the sidelines.

Read more Nonprofits and brands are navigating the partisan air of the 250th in search of a unifying tone

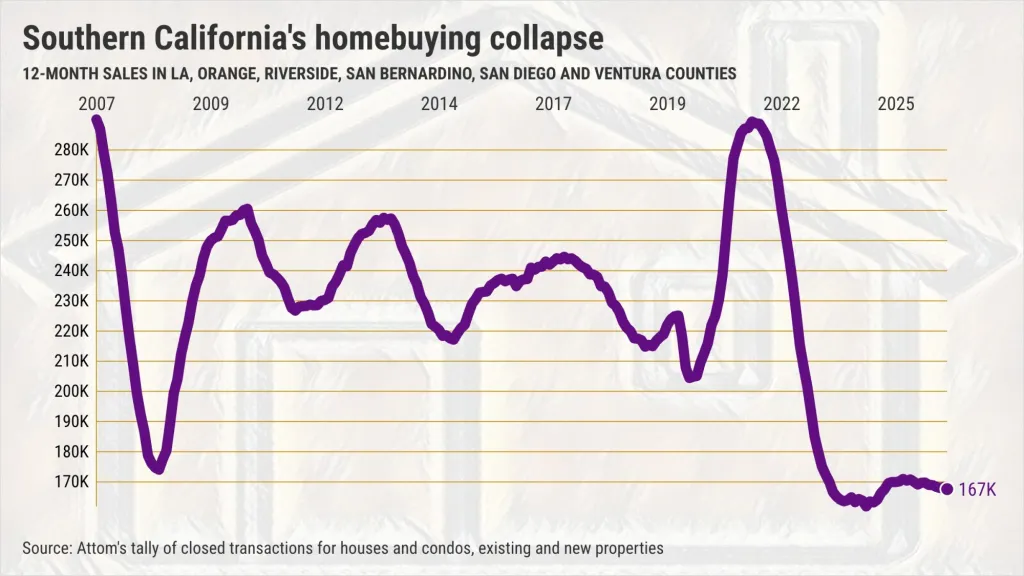

My trusty spreadsheet reviewed a sales report from Attom for April that showed 15,283 sales of houses and condos, existing properties and newly built ones, in Los Angeles, Orange, Riverside, San Bernardino, San Diego and Ventura counties.

That’s 4% fewer sales than last April. In fact, since 2005, only three Aprils have been slower: 2020, when the pandemic hit, and 2023 and 2024, as the market adjusted to the end of the Federal Reserve’s easy-money policy.

Yes, local homebuying remains slower than the depths of the bubble-bursting Great Recession. And this is no one-month blip. Consider 12 months’ worth of activity.

In the last 12 months, 167,500 residences were sold in the six counties. That’s 28% below the historic pace and just 4% above the low point set in June 2024.

The price is wrong

Look, sellers refuse to budge on pricing despite all the economic anxieties.

Not many Southern Californians are willing to swallow April’s $825,000 median price tag. That’s the second-highest ever, just 1% shy of the $831,000 record set in June 2025.

If there’s a silver lining for buyers, it’s that home prices have only crept up 3% over the last four years. For comparison, when the Fed handed out cheap mortgages, local prices shot up 44% from 2018 to 2022.

To me, this is rather simple. Consider the house payment based on Southern California’s $825,000 median sales price, financed at the three-month average mortgage rate of 6.2% in April, assuming a 20% down payment. By the way, rates are around 6.5% in early July.

So, who could afford April’s estimated $4,040 monthly payment to the lender, plus property taxes, insurance, association fees and maintenance? And don’t forget, you’d need $164,000 in cash for the down payment to get these loan terms.

Sure, that monthly payment is down 7% from its peak in May 2024. But this burden is still 32% higher than four years ago, and a whopping 94% more than in 2018.

Curiously, having a landlord looks very affordable. The typical Southern California rent in May was $1,934 monthly for a one-bedroom unit and $2,365 for a two-bedroom, according to ApartmentList.

So, why?

Let’s look at what’s making Southern Californians hesitant to make big purchases, especially a home.

It’s not some complex analysis your favorite real estate guru might offer up.

Foremost, you need a job to buy a house. And with job growth in Southern California running 92% below its 10-year average in May, a steady paycheck is a real concern.

Read more UK sanctions Russian labs and people over chemical weapons used on Navalny and Skripal

Plus, falling demand for workers equals smaller raises. Paychecks in Southern California are growing at their slowest rate since 2018.

This makes balancing a family budget even harder as Southern California inflation popped. Consumer prices rose at the fastest pace of the year in May, as the war in Iran boosted gasoline prices.

So, when the economy is this feeble, it’s no wonder buyers are pulling back from grossly overpriced housing.

How overvalued? According to John Burns Research, Orange County home prices were 35% higher than what the local economy supports, making it the second-most overpriced market in the country.

San Diego and the Inland Empire were 25% overvalued, and Los Angeles was at 19%.

The nation? 26% overpriced – so this is more than a local affliction.

Locally speaking

Look at how the slide in homebuying has varied across Southern California, with the six counties ranked by the size of the fall.

– San Bernardino: 19,600 sales in the year through April were 35% below average – and the lowest in data dating to 2005. April’s $529,000 median – the 11th-highest in 22 years – was 4% below the $549,000 high set in October 2024. And the estimated payment has soared 104% since 2018.

– Riverside: 28,300 sales, 30% below average and only 2% away from March 2008’s low. Pricing? $595,000 median – No. 22 highest – is 3% below April 2025’s peak. The $2,911 payment has rocketed 95% since 2018.

– San Diego: 27,200 sales, 27% below average and 8% away from June 2024’s low. Pricing? $910,000 median – No. 2 highest – 0.4% below June 2024’s peak. Payment? Pumped up 96% since 2018.

– Los Angeles: 61,200 sales, 25% below average and 5% away from June 2024’s low. Pricing? $899,250 median – No. 8 highest – 2% below June 2025’s peak. Payment ballooned 84% since 2018.

– Orange: 24,100 sales, 25% below average and 7% away from May 2008’s low. The record $1.23 million median topped the old high of $1.22 million in March 2026. Payment skyrocketed 114% since 2018.

– Ventura: 7,000 sales, 24% below average and 13% away from June 2024’s low. Pricing? $875,000 median – No. 3 highest – is 2% below June 2025’s peak. The payment soared 81% since 2018.

Jonathan Lansner is the business columnist for the Southern California News Group. He can be reached at [email protected]

Read more Ukrainian midrange drones reshape the battlefield by targeting Russian supply lines

- Try Jonathan Lansner’s Substack collection of economic trends. CLICK HERE!