Only one large U.S. housing market has more out-of-whack home pricing than Orange County.

Read more Kroger buying regional grocer and pharmacy retailer Giant Eagle in deal valued at $1.65 billion

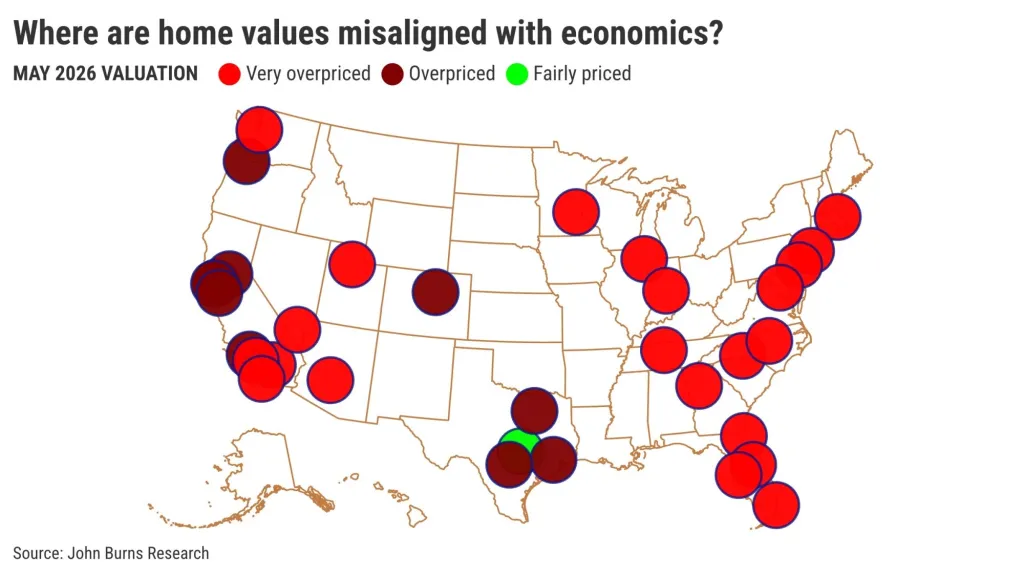

That worrisome trend was revealed in a study by John Burns Research and Consulting, which examined the historical relationships between prices, mortgage rates and incomes as of May in 33 major U.S. housing markets – including eight in California.

Orange County pricing was estimated to be 35% too high relative to its underlying economic fundamentals. Only Indianapolis homes at 42% were more overvalued, a signal that even in the lower-priced Midwest, housing values make little monetary sense.

Now, numerous real estate gurus like to suggest that anyone who’s describing a sickly housing market has little credibility. But these numbers come from one of the most respected research shops in the industry.

So contemplate these stats showing the typical U.S. home is priced 26% above a house hunter’s long-term purchasing power. To John Burns, anything above 20% is in “very overpriced” status.

Curiously, my trusty spreadsheet found that housing in much of California was less overpriced relative to homebuying fundamentals than in other parts of the nation.

The median overvaluation of the eight Golden State markets was 18%. That’s well below the 25% pricing overvaluation in the 25 markets outside the state.

This misalignment shows up in the marketplace as a standoff between what sellers demand and what buyers can pay. This affordability chasm has put home sales in crash mode for four years.

Read more Frumpy Mom: Will your kids be safe at Disneyland?

How unaffordable?

Who can buy at these prices?

Well, the California Association of Realtors estimates that only 22% of Golden State households would qualify to buy the $843,000 median-priced single-family home in the first quarter of 2026. And that feat requires a $205,000 household income – plus a 169,000 down payment.

The only good news: Affordability is up from 19% a year earlier.

Nationally, 44% of Americans can afford the $404,000 national median-priced house – with a $98,000 income required. Affordability was 40% in the first quarter of 2025.

The grand question: What combination of house construction, more owners selling, cheaper mortgages, higher incomes – and, yes, price cuts – will it take to revive homebuying?

Mispriced markets

Consider the overvaluation levels for the seven other California markets in the study, in order of their national ranking:

– San Diego: 25% overvalued, No. 14 of 33.

– Inland Empire: 25% overvalued, No. 14.

– Los Angeles County: 19% overvalued, No. 23.

– San Jose: 17% overvalued, No. 26.

– San Francisco: 16% overvalued, No. 27.

– Sacramento: 16% overvalued, No. 27.

– East Bay: 11% overvalued, No. 31.

By the way, price cuts work magic.

The nation’s least overvalued market – the only one deemed “fairly priced” by the analysis – was Austin. The Texas city, which has seen home values slashed as economic growth cooled, has prices deemed only 6% too high.

Jonathan Lansner is the business columnist for the Southern California News Group. He can be reached at [email protected]

Read more OC beach cities report dogs on beaches are among the highest cause for citations

- Try Jonathan Lansner’s Substack collection of economic trends. CLICK HERE!