If Walmart and McDonald’s can see that high prices are scaring off customers and quickly turn around and offer significant discounts, maybe California’s homebuying world should take a hint.

Read more Sam Neill, New Zealand actor who starred in ‘Jurassic Park’ and ‘The Piano,’ dies at 78

For nearly four years, California house hunters have been saying ‘no thanks’ to sky-high prices. It turns out, even the cash registers at Walmart and McDonald’s are now feeling a similar chill.

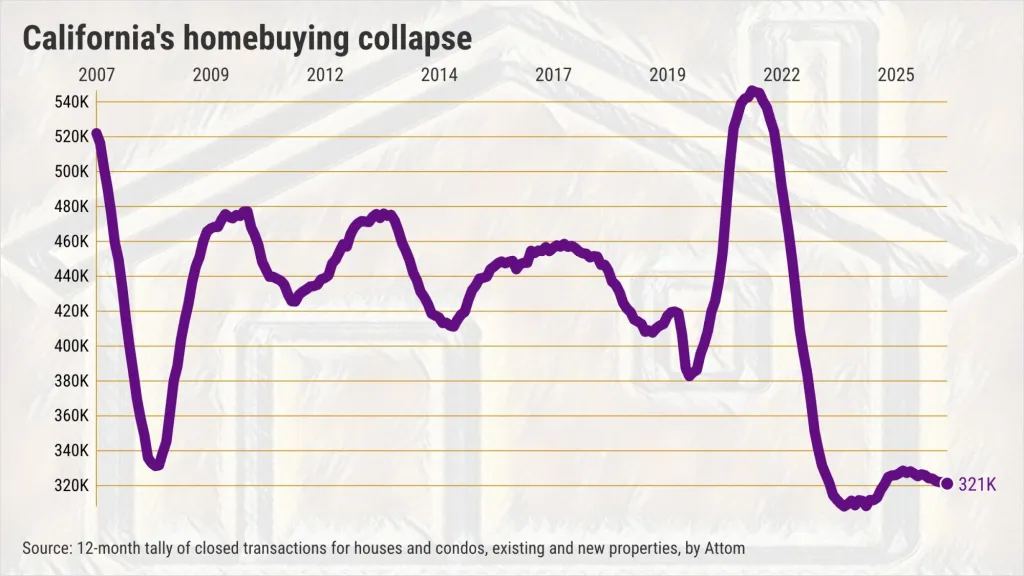

My trusty spreadsheet looked at a homebuying report from Attom showing that in the 12 months through April, there were 320,900 statewide sales of houses and condos, existing properties and newly built.

How slow is that?

Homebuying is running 26% below the historic pace, just a smidgen above the low point set in December 2023, according to data going back to 2005.

The price is wrong

Plenty of housing experts claim the market is just fine because prices are still high. But that logic doesn’t quite add up.

Yes, April’s $748,000 statewide median is the fifth-highest price in California history. And it’s only $3,000 off the all-time high set in June 2025.

However, the sales crash tells us that something is wrong.

California’s homebuying pace has been below average since November 2022, shortly after the Federal Reserve ended its cheap-money era.

Or look at it this way: People are buying 3% fewer homes than during the darkest days of the Great Recession.

Time to rethink

Of course, there are plenty of hurdles for homebuyers besides the sticker price.

There’s a wobbly job market and stubborn inflation, which make paychecks uncertain and diminish buying power. Did I mention a war? All of these factors cut into consumer confidence.

But these are very much the same hurdles faced by Walmart and McDonald’s. The big retailer just cut prices on 7,000 items while McDonald’s is offering aggressive combo meal promotions.

So, maybe homebuilders should ponder rethinking their cost structure, if growing home sales is their goal.

You see, waiting for some sort of bailout – interest rate cuts from the Federal Reserve or another down payment assistance program – is ignoring key underlying challenges for house hunters.

Start with potential sellers.

Note a recent study by John Burns Research and Consulting that shows how much California prices are disengaged from their economic realities: Orange County homes are priced 35% too high, by their math. San Diego and the Inland Empire are 25% overvalued, Los Angeles, 19%, San Jose, 17%, San Francisco, 16%, Sacramento, 16% and the East Bay, 11%.

It’s not just property owners. Perhaps the industry should also chip in to the cost cuts. Housing sellers and lenders should trim their prices. Yes, commissions and mortgage fees are too high.

Read more Who could replace Lindsey Graham? South Carolina’s next steps after senator’s death

Maybe builders could stop targeting the high-end market, too.

More construction would help, but remember that California added half a million new homes over the past eight years as its population essentially stagnated.

Also, please stop suggesting that house hunters overpay because housing is a purportedly great investment.

California home prices have lost momentum across much of the state. The statewide median in April was up only 9% during the last four years. It rose 50% in 2018-22.

Who can buy?

Homes remain unattainable because homebuying has sadly become a luxury game.

The noteworthy wealth of a modest flock of Golden Staters is what creates buyers.

For starters, consider the estimated house payments on the $748,000 median-priced home at April’s 6.2% mortgage rate, assuming a 20% down payment.

Yes, California’s $3,660 monthly payment is 8% below June 2024’s peak – but it’s also up 88% in the past eight years.

And this estimated burden does not include property taxes, insurance, association fees or maintenance. Did I mention the $146,000 in cash for a down payment?

Or think about the California Association of Realtors’ affordability math.

For the first quarter of 2026, the trade group estimated that 22% of California households earn enough to qualify to buy a typical home.

And you’ll need a $205,000 household to meet this financing threshold.

Now travel back to 2019, before the pandemic upended real estate.

In that long-forgotten era, 33% of Californians qualified by CAR’s math – that’s not great either but it’s better. It would also take a $115,000 income to make a deal pencil seven years ago.

Here’s why California housing needs all sorts of discounts: Whose paycheck grew 78% in seven years?

By the way, the price of a Big Mac has risen only 31% since 2019, according to Burgernomics.

Jonathan Lansner is the business columnist for the Southern California News Group. He can be reached at [email protected]

Read more Pilot killed after aircraft fighting wildfire crashes into Colorado reservoir

- Try Jonathan Lansner’s Substack collection of economic trends. CLICK HERE!

0